At Mello Workshop 2015 I spoke on how to construct a high-yield portfolio and documented the process; in this article I create just such a portfolio and discuss some of the questions that arose while following the rules.

Introduction

The first step towards selecting shares for a high-yield portfolio (HYP) is to create a shortlist of companies worth considering. I've used many screening providers in my time, such as Digital Look, but in this case I've put together a very basic filter on Stockopedia:

The reason for keeping it so simple is that all websites have some level of data error and odd values sometimes creep in (such as a forecast yield of zero for HICL Infrastructure when it's been yielding near 5% for years). It's also very easy for me to export the results to a spreadsheet and manually remove low-yielding shares and other unattractive companies (such as foreign entities with a secondary listing in London).

With this spreadsheet (available here in hand I've created a portfolio, of 25 shares, by working down from the very largest companies and considering a few key points:

- is their yield greater than that of the FTSE (roughly 3%)?

- are they in a sector which doesn't already have a selection?

- do they have a reasonable dividend history?

- are they in a reasonable financial state without carrying excess debt?

- are they in a stable or improving sector of the economy?

So without further ado let us move onto the first 15 shares which make the cut right now; the remaining 10 shares are covered in my follow-up article. The reason for this split is that fifteen companies provide the minimum sensible level of diversification for a portfolio and I feel that this blog post is long enough already!

The portfolio (shares 1-15)

1) Royal Dutch Shell [Energy - Oil & Gas]

The largest company in the FTSE, at a hefty £120bn, Shell is forecast to yield almost 6.5% this year and has an average 5-year yield of over 5%. The cover on this payout isn't great, at around 1.3, but Shell hasn't cut its payout in living memory and has the financial firepower to maintain its dividend even in the face of a much reduced oil price. In fact the gross gearing level of 26% is one of the best in the stock market and stands at roughly half of the level for BP (which yields just under 6%). With such outstanding metrics, and no other competition in the Oil & Gas sector, this is a sure-fire selection.

Looking at the dividend policy for Shell it's pretty terse: "Our policy is to grow the US dollar dividend in line with our view of the underlying earnings and cash flow of Shell". In my view this suggests that dividend growth is likely to remain subdued, with the forecasts below supporting this, and any increase in sterling dividend will be down to a strengthening greenback as much as the company (since Shell reports in dollars). That said the first-quarter dividend just paid came in at 30.75p and so Shell is on track for its 2015 forecast payout.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 1870 | 139.2 | 123.5 | 6.60 | 1.13 |

| 2016 | 1870 | 177.7 | 124.0 | 6.63 | 1.43 |

2) HSBC [Financials - Banking Services]

Banks haven't been great investments over the last decade but in the great crisis HSBC was one of the few banks, along with Standard Chartered, to avoid near-nationalisation and a total destruction of shareholder value. More importantly while the dividend was savagely cut at the time it has since rebounded strongly, over the last five years, and is forecast to yield around 5.5% this year with a decent level of cover. While debt is a meaningless ratio with banks, as debt is their business, it's clear that HSBC is working hard to improve its lending ratios and cut costs on a global scale. The only other banking institution that comes close to HSBC is Standard Chartered but with a lower yield and a fifth of the market cap it's out of the running here.

From a strategy viewpoint HSBC's statement is light on detail but does at least imply growing dividends in some manner: We are committed to delivering a progressive dividend. The progression of our dividend should be consistent with the growth of the overall profitability of the Group and is predicated on our ability to meet regulatory capital requirements in a timely manner. It's worth noting that while the company is paying a first quarter dividend of 10c (unchanged from 2014) this fits in with their pattern of loading any increase onto the final dividend: The Directors of HSBC Holdings plc have declared a first interim dividend .... in accordance with their intention to pay quarterly dividends on the ordinary shares in a pattern of three equal dividends with a variable fourth interim dividend. So far so good this year then.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 590.8 | 52.9 | 32.8 | 5.54 | 1.61 |

| 2016 | 590.8 | 55.4 | 34.0 | 5.76 | 1.63 |

3) Unilever [Consumer Defensives - Household Products]

Unilever supplies food, home and personal products that many of us use every day; in this sense it's a very defensive stock and this shows in its earnings and share price history. While it suffers from the effects of inflation and exchange rate fluctuations, which both impact raw material prices, Unilever boasts an excellent record of steadily growing dividend payouts (back to 1999). As a result of this attractive consistency it offers a relatively low yield of 3.1% but this is sufficient to make it into my selection; it's not necessary for every share to be an ultra-high yielder so long as the portfolio as a whole yields decently in excess of the average for all companies in the market.

While I haven't managed to locate an explicit policy on the Unilever website there is a short message on strategy in the 2014 Annual Report: Our financial growth model is based on applying all the levers of value creation. Underlying sales growth, core operating margin improvement and efficient financial management all contribute to growth in earnings per share and free cash flow, from which we pay dividends to our shareholders or reinvest in the business. We aim for these dividends to be attractive, growing and sustainable over time. The only problem with these dividends is that they're declared in Euros and if this continues to weaken against Sterling then our received dividends will decline. Even so I find Unilever worth having at the current share price.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 2772 | 135.4 | 87.8 | 3.17 | 1.54 |

| 2016 | 2772 | 145.4 | 93.6 | 3.38 | 1.55 |

4) BHP Billiton [Basic Materials - Metals & Mining]

Even after demerging a large amount of non-core assets into South32 BHP Billiton remains a formidable, £70bn company with an enviable track record (no cut since 1988) of paying dividends. Despite volatile earnings, as resource prices have suffered with the global economy, BHP Billiton has consistently raised its well-covered dividend and is now paying out over 6%. This is well in excess of any other large-cap mining outfit, such as Rio Tinto, and comes attached to a gearing level below 40%.

That said the company's policy (The aim of this policy is to at least maintain or steadily increase our base dividend in US dollars terms at each half-yearly payment) is the cause of some discussion over whether it's appropriate for a cyclical enterprise. My view is that BHP Billiton has demonstrated remarkable resilience across all market conditions, benefits from an unstressed balance sheet and pays an excellent yield; a great combination for any HYP and qualities worth including.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 1325.5 | 90.1 | 78.75 | 5.94 | 1.14 |

| 2016 | 1325.5 | 66.2 | 78.75 | 5.94 | 0.84 |

5) Vodafone [Telecoms - Telecommunications Services]

Vodafone is a good example of an apparently dividend-cutting company that remains a decent HYP choice; in this case with the sale of its huge stake in Verizon the company rebased its shares to reflect the change. Unfortunately some data providers haven't updated their records to reflect this even though the dividend history on the company website shows a 15-year record of inflation-beating increases. Right now the yield is around 4.5%, which is reasonable, and the gearing level is a remarkable 53%; for a utility-like company this is as close to debt-free as you can find! As a result none of the other candidates in the sector, such as BT, are worth considering.

Frustratingly Vodafone is another company without an explicit dividend policy but they do have this to say in the recent Annual Report: "Although cash flow will continue to be depressed in the coming year given the high levels of investment, our intention to continue to grow dividends per share annually demonstrates our confidence in strong future cash flow generation". This sounds consistent with the company's post-Verizon actions of investing for the future at the expense of current profits - which also, possibly, explains the low earnings forecasts for 2016/2017. I have no idea how accurate these predictions will turn out to be but such guessing is outside of the HYP process; in all other ways Vodafone hits the mark.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2016 | 233.65 | 5.26 | 11.5 | 4.92 | 0.46 |

| 2017 | 233.65 | 6.07 | 11.6 | 4.96 | 0.52 |

6) British American Tobacco [Consumer Defensives - Food & Tobacco]

While some investors harbour ethical concerns over tobacco companies there's no doubt that they make phenomenal HYP shares. BAT has employed its huge free cash-flow to power inflation-busting dividend rises for many years and there's no sign of this investor-friendly approach slackening off. Right now BAT is yielding 4.4%, with decent coverage, and this is a pretty typical yield historically. The only factor that puts me off BAT is its very high gearing level, of 222%, but in my view this is a reflection of management actively reducing the capital base required to sustain operations rather than a sign of an over-leveraged enterprise.

An aspect of BAT that I admire is that their dividend policy is very straightforward: "The Group’s policy is to pay dividends of 65 per cent of long-term sustainable earnings, calculated with reference to the adjusted diluted earnings per share. Interim dividends are calculated as one-third of the total dividends declared for the previous year". Given how the board have managed to grow these earnings, via organic growth in emerging markets and targeted acquisitions, I can see why analysts are forecasting above-inflation dividend growth for the next few years.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 3547 | 209.6 | 155.1 | 4.37 | 1.35 |

| 2016 | 3547 | 226.7 | 163.6 | 4.61 | 1.39 |

7) AstraZeneca [Healthcare - Pharmaceuticals]

AstraZeneca is an interesting selection as it's the first time, in this portfolio, where I've skipped a larger, higher-yielding company (GlaxoSmithKline) in favour of its smaller shadow. This wasn't an easy decision but for me the key points are that GlaxoSmithKline supports a substantially higher gearing level (248% vs 62%) and broker forecasts of dividend cover suggest a payout under greater pressure (1.1 vs 1.5). So I see AstraZeneca's yield of 4.2% as being more sustainable than GlaxoSmithKline's 5.8% and, as we know, the art of HYP construction is to choose companies that minimise the risk to our portfolio income.

From a policy perspective AstraZeneca strikes an appropriate note: "The Board has adopted a progressive dividend policy, intending to maintain or grow the dividend each year but, recognising that some earnings fluctuations are to be expected, the annual dividend will reflect the Board’s view of the earnings prospects over the entirety of the investment cycle". In practice this allows for quite a lot of wiggle room as the dividend history shows; in dollar terms the payout has been static for 4 years and the sterling amount has dropped due to exchange rate effects. In time I hope that AstraZeneca is able to grow the dividend once again but meanwhile the payout doesn't look under threat.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 4189 | 267.1 | 177.0 | 4.22 | 1.51 |

| 2016 | 4189 | 263.3 | 176.4 | 4.21 | 1.49 |

8) Diageo [Consumer Defensives - Beverages]

This is another share where I've skipped a larger compatriot, SABMiller, but here the choice is straightforward; Diageo's yield is low at 3.0% but SABMiller's is positively sub-zero at 2.3%. In other respects they are quite comparable with excellent records of increasing dividends, sensible cover from earnings and dominant positions around the globe. The only fly in the ointment with Diageo is that its debt load has been increasing for a number of years, due to expansion by acquisition, and its gearing level of 157% is definitely in uncomfortable territory. That said the interest cover from earnings is very good and Diageo doesn't appear to be struggling with this level of liabilities.

From a historical perspective Diageo has been a steady payer of dividends for long-term holders; the dividend has risen every year since 1998 and possibly even back to 1989. So it's curious that the company neither trumpets this fact nor publicises a dividend policy. The closest thing that I can find to a statement are these answers to questions on the 2009 results! Here it is suggested that an annual growth rate of 5%, and a dividend cover of around 2, is 'appropriate'; this certainly holds true for 2009-2011 although in recent years the increases have usefully jumped to around 9%. This is a decent result with or without a known policy.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 1907 | 90.4 | 54.0 | 2.74 | 1.67 |

| 2016 | 1907 | 96.6 | 57.6 | 3.02 | 1.68 |

9) National Grid [Utilities - Multiline Utilities]

In order to reach National Grid I've skipped over the seven companies between it and Diageo with barely a second look; in each case they're either in a sector already covered or their yield is markedly below 3%. With National Grid though this is the first true 'utility' in the sense of a heavily regulated service supplier that maintains a large and critical infrastructure; the advantage of regulation is that earnings growth is often fixed in advance but with the downside that very large amounts of debt exist and need servicing. As such the reasonably covered yield on offer, of 5%, has to be set against gearing of 216%. Ultimately, though, National Grid has a very explicit plan for paying dividends to shareholders and I think that it makes a sensible addition to any HYP.

This plan, announced back in 2013, states that: The new policy will aim to grow the ordinary dividend at least in line with the rate of RPI inflation each year for the foreseeable future. This is a step back from the previous (and perhaps unsustainable) policy of 4% growth every year and an aside suggests that these days are unlikely to return: Any dividend increases above inflation will need to be supported by sustained outperformance and to have no impact on long-term credit ratings. Notwithstanding this deceleration National Grid still yields handsomely and has maintained a growing dividend since 1996; key HYP qualities for any share.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2016 | 861 | 58.6 | 44.1 | 5.12 | 1.33 |

| 2017 | 861 | 60.2 | 45.3 | 5.26 | 1.33 |

10) Sky [Consumer Cyclicals - Media & Publishing]

This is, perhaps, a more controversial choice than any other share so far. The yield of 3.3% isn't stellar, even compared to others in the same sector like Pearson, but double-digit growth over the last five years has certainly propelled it into HYP contention. From an economic perspective this step-change has been driven by Sky taking control of its content-driven market and achieving excellent cash-flows from its largely captive audience (despite the ever-increasing cost of obtaining this content). Now the gearing is unnervingly high at 300% but this is a legacy of recent, large acquisitions and certain to reduce. In my view then Sky is in a growing market and likely to mature into a core HYP holding.

What's quite instructive is that this wasn't always the case; according to the dividend history Sky paid a maiden dividend in 1995, and kept them up for 4 years, before coming to a grinding halt in 1999. It took until 2004 for the company to pick up the reins again, having been burnt once, although since then we've had 10 years of growth with the payout multiplying by over 5 times. Usefully I've located some guidance on future intent in the shareholder circular issued in late 2014 for the takeover of European operations. In this we learn that: "The Independent Directors intend that the Enlarged Group will maintain a progressive dividend policy ... Following the initial dilution to earnings arising from the Transaction, the Independent Directors expect to return to the Company’s current stated policy of paying out 50% of adjusted earnings as ordinary dividends". So if the acquisition performs as expected then shareholders will be rewarded with continued increases; sounds good to me.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 1074 | 53.5 | 32.5 | 3.03 | 1.65 |

| 2016 | 1074 | 63.5 | 35.0 | 3.26 | 1.81 |

11) BAE Systems [Industrials - Aerospace & Defense]

Another possibly controversial choice is BAE Systems; the weapon manufacturer. Its got a pretty checkered past in the corporate ethics department but from a HYP perspective the dividend history is excellent. With over 15 years of dividend growth in the bag it still remains on a reasonable rating and yields around 4.1% (with cover of 1.8x). Unusually there's another good candidate in this sector, Cobham, which yields 4.0% and so is snapping at BAE's heels. However BAE is five times the capitalisation of its competitor and while the gearing is worse at 182% (compared to 130%) its sheer size makes it the safer pick in this sector.

A possible concern is that BAE fields a number of demands on its finite resources and dividends are just one part of this: "The Group ... plans to pay dividends in line with its policy of long-term sustainable cover of around two times underlying earnings and to make accelerated returns of capital to shareholders when the balance sheet allows". The key point here is that the board are using their own definition of earnings to determine cover and in 2014 (and 2013) these earnings came in at 38p (and 42p); the result being a cover of around 1.85 and a sense that this is in line with the policy. So while I don't expect eye-popping future increases, in this time of defence cutbacks, I do feel that BAE will work hard to maintain its record.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 479 | 38.4 | 20.9 | 4.36 | 1.84 |

| 2016 | 479 | 40.5 | 21.6 | 4.51 | 1.88 |

12) Legal & General (Financials - Investment Services)

There are a lot of options in this sector, which suggests that as a whole it's out of favour, with 14 companies out of the 190 in the full list that I'm selecting from here. However Legal & General stands head and shoulders above the rest, as a HYP share, due to its size (£15.1bn), yield (5.2%), cover (1.4x) and gearing (61%); although it's arguable whether the latter is meaningful in the financial sector. More importantly while Legal & General has cut its dividend twice in recent times (in 2007 and 2008) its track-record over more than 15 years is exemplary and the current dividend is twice the pre-cut dividend of 5.97p. So all-round this company has delivered for the long-term investor.

That said the company provide a rather interesting graph which incontrovertibly shows that the dividend will not continue to rebound at this double-digit rate. There has been a catch-up phase while the cover returns to about 1.5x: "We announced new dividend guidance in 2014. Should our Solvency II surplus be no lower than Solvency I, we expect that we will move towards returning two thirds of net cash to shareholders via dividends. (1.5 times cover) by the end of 2015". With earnings growth for the next few years forecast to barely break double digits this will inevitably limit headroom - although a yield of 5% is not to be sniffed at. Whatever happens it's likely that the board will revisit this issue later in the year: "We will provide updated dividend guidance when Solvency II clarity has fully emerged. The Board remains committed to a progressive dividend policy over the long term".

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 258.4 | 18.8 | 13.0 | 5.03 | 1.45 |

| 2016 | 258.4 | 20.5 | 14.3 | 5.53 | 1.43 |

13) Next (Consumer Cyclicals - Speciality Retailers

Next, the clothing and houseware retailer, is not a typical HYP choice and for a very good reason; its ordinary dividend leaves it yielding barely more than 2%. What makes Next transcend this is that in the last year it has moved from buying back shares to issuing regular and sizeable special dividends - sufficient to double the yield to over 4%. Alongside this Next has an impressive fifteen-year dividend history, with no cuts, and excellent cover of around 1.5x. The only, apparent, weakness with Next is its astronomical gearing of 261% but this is a conscious decision by the board; the equity base of the company has been whittled away by share buybacks, making the £565mn of debt look worse than it is, while so much free-cash is generated by the business that interest payments are a minor issue.

A quality that I particularly admire with this company is that management are quite clear on who they work for and why: "The primary financial objective of the Group is to deliver long term returns to shareholders through a combination of sustainable growth in earnings per share (“EPS”) and payment of cash dividends". As part of this they present a very coherent description of when they feel share buybacks are appropriate and when they don't add sufficient value. Right now the share price is almost 10% above the upper limit for buybacks (of £68.27) and so it's likely that this statement will play out in practice: "We expect to generate around £360m surplus cash in the year ahead and, again, we intend to return this to shareholders. We paid a £74m special dividend in February and have committed to a further £90m which will be paid in May. If our share price remains above our maximum limit for buybacks and our profit expectations remain unchanged, then we intend to pay further quarterly special dividends in August and November this year".

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2016 | 7475 | 430.7 | 308.3 | 4.12 | 1.40 |

| 2017 | 7475 | 458.5 | 312.9 | 4.19 | 1.47 |

14) Pearson (Consumer Cyclicals - Media & Publishing)

Sharp-eyed readers will have spotted that this is, shock horror!, a duplicate sector; we already have Sky in the portfolio so why is Pearson up for consideration? Well in my view the standard sectors are a guide (and a good one) but no more than that; quite regularly very different companies end up lumped together in the same sector despite their economic exposure being uncorrelated and this is a case in point. Pearson is an international education and publishing company, yielding 4.2% and boasting a fine dividend history, while Sky is a European television broadcaster with broadband and telephone sidelines; so they're very different. Also Pearson enjoys low gearing of 37% and decent dividend cover of 1.5x. So in this case I'm happy to include a second company in the same apparent sector as they're sufficiently diversified to provide the income protection that we're looking for.

An attractive element of this share is that management are rightfully proud of the company's dividend record: "An increase in our dividend of 6% .... which was Pearson’s 23rd straight year of increasing our dividend above the rate of inflation. Over the past ten years we have increased our dividend at a compound annual rate of 7%, returning £2.9bn to shareholders". The only problem with such a history is that it can encourage directors to over-distribute during lean years and I think that this risk is alluded to here: "We have a progressive dividend policy: we intend to build our dividend cover to around 2.0x over the long term, increasing our dividend more in line with earnings growth from then". My interpretation of this is that future increases are likely to be subdued given a current dividend cover of 1.5 or so but that's no real hardship when starting from a yield of 4%+.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 1272 | 77.8 | 54.6 | 4.29 | 1.42 |

| 2016 | 1272 | 83.4 | 57.4 | 4.51 | 1.45 |

15) United Utilities (Utilities - Water Utilities)

Utilities are often viewed as the stalwarts of any HYP with their generally high yields and secure, regulated income stream. However in recent years a certain amount of takeover mania has emerged in this sector - the result being that there are fewer companies to choose from, compared to a decade ago, and the yields on offer are rather compressed. Hence United Utilities yields barely 4%, covered an unimpressive 1.1x, while simultaneously shouldering a hefty 273% gearing. For any ordinary firm these numbers would be an instant turn-off but the saving grace is that utility companies provide significant diversification and United Utilities is another enterprise with a reasonable 25-year payout record.

However I do feel a certain level of concern over how close to the wind the company is sailing with its very low dividend cover and it seems that the board are thinking along similar lines. In the 2010-15 period United Utilities stuck to a policy of targeting a growth rate of RPI+2 per cent per annum. This became something of a challenge and last year they did the absolute minimum: "This is an increase of 4.6 per cent .... the inflationary increase of 2.6 per cent is based on the RPI element included within the allowed regulated price increase for the 2014/15 financial year". For 2015-20 the dividend policy is being substantially watered down: "The board approved a policy of maintaining the existing level of dividend and targeting a growth rate of at least RPI inflation each year through to 2020". Even more than this the director performance targets are switching their focus from dividend growth to dividend cover - a very sensible decision.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2016 | 982.5 | 43.2 | 38.5 | 3.92 | 1.12 |

| 2017 | 982.5 | 43.8 | 39.4 | 4.01 | 1.11 |

Conclusion

With 15 companies in the bag the blended yield across all of these shares is about 4.5% (with a combined cover of 1.4x). This is a very respectable result for a portfolio drawn solely from the very largest companies in the UK market with a specific focus on dividend resilience and longevity.

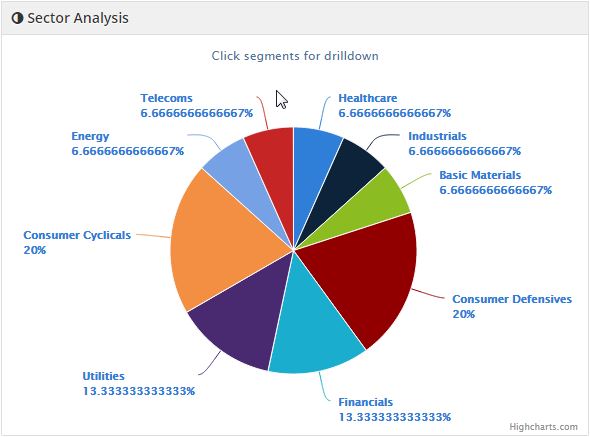

Looking at the sector allocation, which should be evenly spread by design, the weighting looks acceptable for the purposes of risk reduction and diversification. The two top-level sectors which stand out are Consumer Defensives and Consumer Cyclicals; the former holds ULVR, BATS and DGE while the latter contains SKY, NXT and PSON. While these are all dependent on the private customer they all also occupy quite different market verticals and so aren't exposed to quite the same economic and legislative risks:

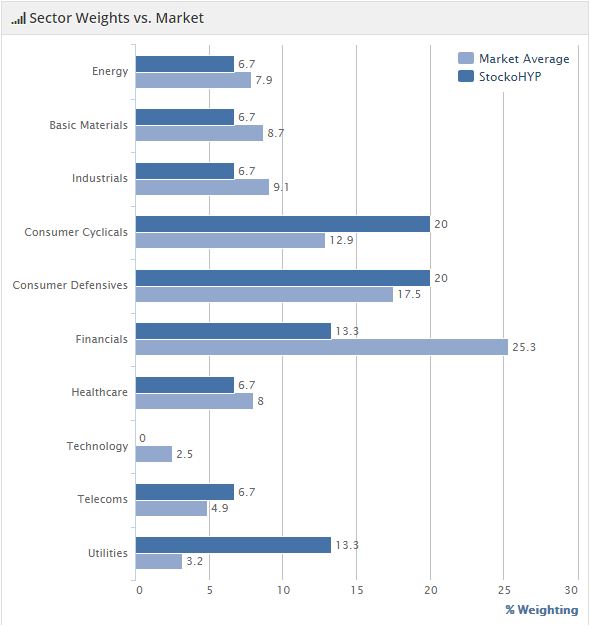

It's also possible to compare these allocations to the market as a whole and this is quite informative. While some of the sectors are quite similar, such as Energy and Healthcare, overall it's clear that this HYP isn't a closet-tracker and doesn't share the markets concentration in some areas (such as Financials). This is another way in which the HYP isn't correlated with the wider stock market and shouldn't track the gyrations of the market directly:

The next step is to increase the number of holdings to 25 (to further reduce risk and exposure to any single sector); this is done in Part 2.

Disclosure: The author holds almost all of the shares mentioned in this article.