At Mello Workshop 2015 I spoke about how to construct a high-yield portfolio and documented the process; in this article I create just such a portfolio and discuss some of the questions that arise while following the rules.

Introduction

In Part 1 of this article I discuss how to select a shortlist of shares suitable for a high-yield portfolio (HYP) and go on to chose the first fifteen companies. In this follow-up article I expand the portfolio to twenty-five shares and discuss some of the necessary decisions and compromises required with these smaller-scale businesses.

The spreadsheet of all shares considered for this HYP can be found here.

The portfolio (shares 16-25)

16) easyJet (Industrials - Passenger Transportation)

Once you're past 15 shares it can become tricky to find suitable candidates, in novel sectors, and creativity is required; hence my inclusion of Easyjet. The positive aspects of this budget airline are its size (£6.4bn), low gearing (32%), decent yield (3.8%), excellent cover (>2x) and double-digit annual dividend growth over the last 5 years (>30% per annum). The negative aspects are that, well, it's an airline (they always lose money don't they?) and the short history of payouts (just five years). These are certainly significant strikes against the company but on balance I think that it's worth gaining exposure to this growing sector and trusting that management will continue to execute profitably.

With the maiden dividend arriving in only 2011 it's important to check just why management started paying them (excess capital on the balance sheet it appears) and, more crucially, what their intentions are. Four years ago this was to "Target consistent and continuous payments", with a limit of "Five times cover, subject to meeting gearing and liquidity targets", and this remains true today. However improved performance means that the payout target has been lifted to: "40% of profit after tax pay-out ratio for ordinary dividend" with the possibility of special dividends to return excess capital. So it's clear that Easyjet intends to continue rewarding shareholders appropriately - in stark contrast to most other airlines.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 1596 | 127.5 | 59.0 | 3.70 | 2.16 |

| 2016 | 1596 | 141.9 | 59.9 | 3.75 | 2.37 |

17) Smiths (Industrials - Industrial Conglomerates)

Smiths Group is a global technology company that covers everything from healthcare to telecoms but that's not the major attraction here; what really captures my attention is a dividend history stretching back to 1994 with no cuts whatsoever. This suggests to me a corporate culture of consistent profitability and shareholder focus. At the present time this means a well-covered (2x) dividend and a yield of 3.5%; both of which are quite adequate. The gearing is a little high at 90% but this is more a result of this being a capital-light company than of too much debt on the balance sheet; a conclusion bolstered by a solid 7x interest cover. Finally there are no other candidates in this sector anyway and so Smiths Group makes it into the portfolio.

Looking again at the remarkable track record of Smiths Group I'm struck by just how consistently and reliably this company has managed to reward shareholders over more then two decades. The worst charge that can be levelled at the group is that they held their dividend at 34p for four whole years (2007-2010) during the worst recession since WWII. I only wish that every HYP share could perform so badly! When it comes to the future Smiths Group has a healthy regard for its owners: "The Board has a progressive dividend policy for future payouts while maintaining a dividend cover of around 2.5 times over the medium term. This policy will enable us to retain sufficient cash-flow to meet our legacy liabilities and to finance our investment in the drivers of growth. While the medium-term objective is to maintain this dividend cover, we will operate some flexibility in applying the 2.5 times cover to take account of short-term impacts such as foreign exchange. This is in order to underpin progressive returns to shareholders". So I have no concerns about the company as part of this HYP.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 1148 | 80.0 | 41.0 | 3.57 | 1.95 |

| 2016 | 1148 | 81.3 | 41.7 | 3.63 | 1.95 |

18) Berkeley (Financials - Real Estate Operations)

During the financial crisis house-builders suffered terribly as the property market nose-dived and previous acquisitions of over-priced land led to huge write-offs and losses; dividends were an obvious victim. That pain is, however, in the past and companies like Berkeley Group are making higher than ever profits and sit in a position to reward shareholders. In this particular case though the payout structure is rather unusual; the company plans to return £13 in the years up to 2021 with a target of returning £4.33 in each three-year period (to 2015, 2018 and 2021). So far Berkeley Group has paid out £3.44, in the 2015 period, and is forecast to pay out a final 90p in the Autumn.

Now given that this dividend is sensibly covered (1.5x), the company has no debt and a plan which implies an annual yield of 4.6% then there's an awful lot to like about Berkeley Group. Of course the dividend history is a wreck, with no dividends being paid for a full 8 years, but in my view management offset this by putting themselves on the hook for almost a decade - and for very sensible reasons: "This puts in place a framework which allows Berkeley to operate at its natural size and to optimise returns to shareholders while managing the risks of a cyclical market.". Outside of fixed-interest bonds it's almost impossible to procure such a known future payout and for this reason I think that Berkeley Group is worth a shot.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2016 | 3389 | 239.9 | 153.7 | 4.54 | 1.56 |

| 2017 | 3389 | 347.5 | 154.8 | 4.57 | 2.24 |

19) IMI (Industrials - Machinery, Equipment & Components)

IMI is another specialist engineering company but their niche involves precision valves and actuators. More pertinently they make very good returns in this field and have comfortably paid well-covered dividends for almost 20 years (or as far back as I have data anyway) with a bit of a growth spurt in the last few years. The yield isn't too exciting at just 3.3% but it is above the index average (the important bit) and only one other company in the sector, Weir, yields above 2.3% (just). Also debt isn't an issue here with gearing of 48% and I get the feeling that IMI is run conservatively enough to ensure that this remains the case. The only other concern is that IMI doesn't diversify away from Smiths Group but I can find no evidence of this beyond the fact that they both make things!

Usefully IMI is quite forthcoming about how it manages its capital structure and financing costs; it's surprising how unusual it is to find this level of detail in an annual report. From our perspective the important bit is this section: "The Board supports a progressive dividend policy with an aim that the dividend should be covered by at least two times underlying earnings. In the event that the Board cannot identify sufficient investment opportunities through capital expenditure, organic growth initiatives and acquisitions, the return of funds to shareholders through share buybacks or special dividends will be considered". This sounds pretty positive and I can see IMI chugging along with its low but acceptable yield for many years to come.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 1163 | 74.1 | 39.4 | 3.39 | 1.88 |

| 2016 | 1163 | 79.3 | 41.9 | 3.60 | 1.89 |

20) DS Smith (Basic Materials - Containers & Packaging)

I'm impressed that a £3.4bn company can be built out of recycled cardboard but it turns out that packaging is big business and DS Smith is one of the smaller companies in this sector. What's also impressive is that the company has transformed itself from a sleepy outfit (as shown by the flat share price and dividend for 2000-06) into a leaner, expanding company via a substantial business crisis in 2009. At that time the dividend was halved and only last year did the payout manage to breach the high-water mark of 8.8p with a sharply increased (by 25%) 10p distribution. Despite this surge the cover remains good at 2x and while gearing is a touch high at 70% the outstanding debt level is heading in the right direction. So DS Smith serves as a good example of the resilience that we're looking for; every company stumbles occasionally but the ones that survive and prosper are worth having.

The only problem with DS Smith is that its yield is absolutely as low as its possible to go and still remain a HYP candidate. It's only the recent inflation-busting increases and strong dividend policy that tip the balance in this share's favour. As it happens the policy is perhaps a little conservative (in that the company could distribute a greater proportion of earnings) but seems a sensible compromise given the need to service debt: "The Board considers the dividend to be an important component of shareholder returns and, as such, has a policy to deliver a progressive dividend, where dividend cover is between 2.0 and 2.5 times, through the cycle". If management can maintain momentum (and their turnaround in general) then I can see dividends continuing to rise in-line with improving profits.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 390.5 | 24.5 | 11.4 | 2.92 | 2.15 |

| 2016 | 390.5 | 25.7 | 12.0 | 3.07 | 2.14 |

Note: Now we're up to 20 companies and the blended yield is still a handsome 4.3% (with a combined cover of 1.5x). So very little income has been sacrificed to achieve substantially improved diversification and, in theory, this income is slightly more protected by earnings.

21) SEGRO (Financials - Residential & Commerical REITs)

SEGRO is a real-estate trust that deals in industrial property, such as warehouses, and this has two implications; the first is that SEGRO must pay out 90% of its taxable profits in the form of dividends and second it's not exposed to the residential housing market that Berkley covers. Right now this leads to a yield of 3.7%, which is good but not the best in the sector, with a cover of 1.2x. The trump card for SEGRO though is the fact that it has only cut its dividend once in fifteen years (in 2008) and possibly for longer than that; it's unclear from a dividend history that stretches back to 1986 what, if anything, happened in 2000. The other positive aspect of SEGRO is its conservative gearing of 59% although this is par for the course in this sector; it appears that real-estate managers don't want to get burned again by excess debt.

Now ordinarily I'd be concerned by such a low dividend cover but REITs are a special situation for two reasons; the rules require them to pay out a high-proportion of rental profits and property companies are best valued on their NAV (net asset value) rather than earnings. What's interesting is that SEGRO aim to pay out more than the minimum: "Since we also receive income from our properties in Continental Europe, our total dividend should normally exceed this minimum level. In practice, we aim to distribute between 85 and 95 per cent of our EPRA earnings (i.e. earnings from both the UK and Continental Europe) as a combination of PID and ordinary dividend". This is very positive and ties in with the company's goal of "being a leading income-focused REIT". As a part of this aim management also have this to say: "We seek to maintain a stable progression in earnings and dividends over the long term. We have a low appetite for risks to this stability, but are prepared to tolerate fluctuations in dividend cover as a consequence of ongoing capital recycling activity". So I'd say that the board is focused on shareholder interests here - exactly what we're looking for with a HYP share.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 416.8 | 18.2 | 15.5 | 3.72 | 1.17 |

| 2016 | 416.8 | 19.2 | 16.0 | 3.84 | 1.20 |

22) Booker (Consumer Defensives - Food & Drug Retailing)

The food retail sector has long been favoured by high-yield investors with companies such as Tesco and Sainsburys seeming to offer high, sustainable and robust dividend income. Unfortunately deflation and the onslaught of discount retailers, Aldi and Lidl, has wrought devastation across the board. Now these consumer heavyweights aren't about to go bust but they are a shadow of their former selves. Nevertheless I feel that it's worth having some exposure to the FMCG world and Booker provides this without being a direct competitor to the discounters - principally because it's a wholesaler rather than a retailer.

Unfortunately the yield available here is a miserly 2.7%, covered 1.4x times, although this is sweetened by a CAGR (compound annual growth rate) over the last five years of 30%. So the company is putting in a sustained effort to reward shareholders and with no debt on the balance sheet it's certainly in a good position to do so. In fact recent results indicate exactly this with a special dividend being planned: "In addition to the final dividend, the Board is recommending a special capital return to shareholders of 3.50 pence per ordinary share (at a cost of approximately £62m, based on the current issued share capital of the Company). This follows the capital return of 3.50 pence per share to shareholders in July 2014. We currently anticipate returning a similar amount to shareholders in July 2016." That said dividends have only been paid since 2008, with debt reduction being the priority before then, and so this is a higher-risk than normal HYP share.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2016 | 171.9 | 7.26 | 5.17 | 3.01 | 1.40 |

| 2017 | 171.9 | 8.03 | 5.37 | 3.12 | 1.50 |

23) Amlin (Financials - Insurance)

Another sector which has proved profitable for HYPs over the years is that covering non-life insurance and reinsurance. Typically opaque, with arguably even more complex reporting than that of banks, such Lloyds-type syndicates have delivered impressive payout levels although with more volatility than the norm. This is simply because these companies are exposed to large-scale disasters, such as the WTC attacks and Hurricane Katrina, with the result that in some years profits are wiped out and reserves plundered. Nevertheless Amlin has a solid history stretching back to 1994 with the last cut in 2001, a rapid return to the dividend list and multiple special dividends since that time.

Currently Amlin yields an excellent 5.9%, covered 1.4x, and that doesn't include the 15p special dividend paid just last month. There are a number of other companies in this sector, such as the colossal £41bn Prudential, and several deliver a higher yield - but with marginal dividend cover of around 1x which is a disaster waiting to happen. Some of these outfits also boast a lower gearing but at 15% (and reducing) this is hardly a problem for Amlin either. So on the whole I find Amlin to be an attractive HYP investment in a useful sector (which explains why a number of competitors, such as Catlin and Brit Insurance, have been taken over at decent premiums already this year).

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 487.3 | 41.6 | 28.8 | 5.91 | 1.44 |

| 2016 | 487.3 | 41.0 | 30.4 | 6.24 | 1.35 |

24) Greene King (Consumer Cyclicals - Hotels & Entertainment)

By this point in the process we are swimming with the relative minnows who clock in at less than £2bn in size and Greene King is no exception - it's the smallest member of the entertainment sector. Even so it punches above its weight by yielding 3.7%, with only William Hill even coming close at 3.1%, and maintaining a cover of 2x. This is all pretty good but what really seals it for me is that Greene King hasn't cut its dividend since 1997 (the limits of my data source) and has instead increased its distribution every single year since then. This demonstrates remarkable consistency, and dedication to the cause of shareholder returns, but also the benefit of checking primary accounts when examining companies.

The reason for mentioning this is that the web site I'm using here, which is Investorease, suggests that the company cut its dividend at least twice (in 2006 and 2010). However from checking the accounts I know that the first 'cut' was due to a 2-for-1 share split doubling the number of shares and the second 'cut' arose from adjusting for the rights issue carried out in 2009 to reduce debt. So far from being a serial dividend-disappointer Greene King is a solid company with slightly more gearing than I'd like (at 153%). Although with 94% of the estate being either freehold or on a long lease I don't view this as a reason to reject to Greene King - so I haven't.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 866 | 60.5 | 29.7 | 3.43 | 2.04 |

| 2016 | 866 | 65.1 | 31.6 | 3.65 | 2.06 |

25) Berendsen (Industrials - Professional & Commercial Services)

With my final choice we're selecting from one of the most random sectors around; here Experian (credit checking) rubs shoulders with Aggreko (mobile power) and Pennon (water utility). What a motley crew. For what it's worth Berendsen, a specialist cleaning company, offers the best balance of yield (3.1%), cover (2x) and gearing (94%) in this group. In addition a closer look at the historic results indicates that Berendsen hasn't cut its dividend in 25 years and has only held its value twice in that period (although a rights issue in 2002 leads to the appearance of a cut). Clearly this is a profitable and resilient enterprise flying beneath the radar of most investors - which is a positive for any HYP share in my view. So it seems that this portfolio is completing with an archetypal high-yield company (profitable, boring, cash-generating and consistent) which reflects the strength of the process.

In looking for details of Berendsen's dividend policy I came across that old chestnut - the progressive dividend! Now to be fair the board have actually satisfied this goal with the payout growing by around 8% per annum for a number of years (although without quite keeping pace with earnings growth with the result that cover has improved from <1.5x to almost 2x). Hopefully the dividend will catch up in time and the management sound confident about the future: "We have a strong and strengthening balance sheet. We continue to generate cash and we remain committed to paying a progressive dividend. We believe we can achieve our growth plans without any long-term detrimental impact on our returns". As such Berendsen feels like a pretty good company with which to end.

| Year | Price (p) | Earnings (p) | Dividend (p) | Yield (%) | Cover |

|---|---|---|---|---|---|

| 2015 | 1018 | 62.0 | 31.2 | 3.06 | 1.99 |

| 2016 | 1018 | 66.5 | 33.1 | 3.25 | 2.01 |

Note: With the complete portfolio standing at 25 companies I'm happy to report that the blended yield holds up at 4.2% (with a combined cover of 1.6x). So great diversification, and decent income, is possible even when the market as a whole is rather buoyant. In this light there's really no need to try and time the market by waiting for the next crash!

Conclusion

With the portfolio now complete I'm quite pleased with the result and the fact that it proved possible to pick 25 sectors and still achieve an overall yield above 4% with an appropriate level of cover. Beyond this I'm gratified that so many of the constituents have such robust dividend histories and sensible payout policies - even though these aren't part of the selection criteria. While nothing is certain, except that some of these companies will hit problems, I'm hopeful that these characteristics will allow the portfolio to cope with such difficulties without undue damage.

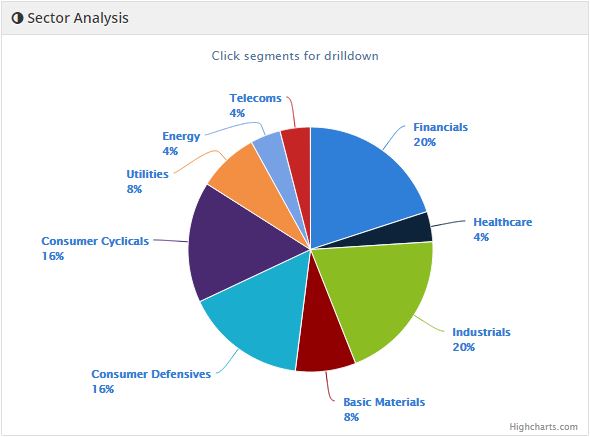

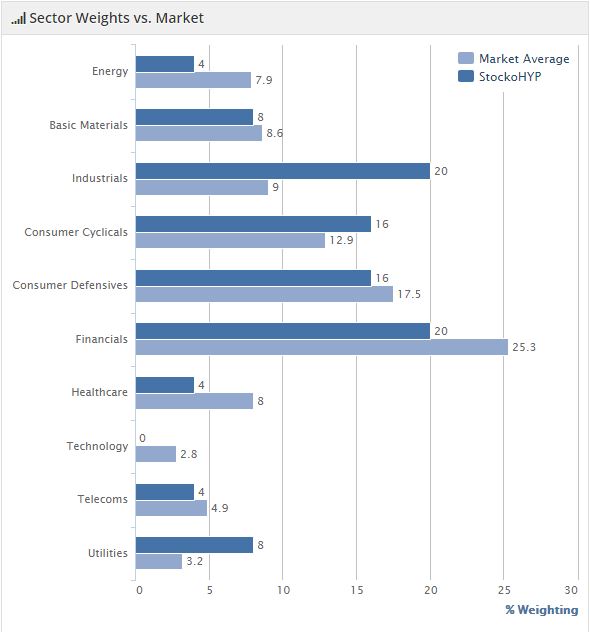

Looking at the sector allocations across the portfolio, where each share has a 4% allocation, then the Financial and Industrial super-sectors do appear rather overweight. However while HSBA, LGEN, AML, SGRO and BKG clearly have a shared reliance on the savings/investment/insurance space I don't view them as overlapping in their business activities and that's the main concern for a HYP; equally the Industrial group includes IMI, SMIN, BA., EZJ and BRSN and the same argument applies. That said it's worth being cautious when deciding whether one company is too close to another as diversification is of key importance for a HYP:

Compared to the market this 25-share subset matches surprisingly well in some sectors (such as Basic Materials or Telecoms) but of course this is pure chance. There's nothing in the selection process that requires a portfolio to be aligned with the wider market and in some ways we're aiming for quite the reverse; where sectors are out of favour (and at a reduced weighting in the market-cap orientated FTSE index) then the constituents of that sector are likely to be on favourable yields. This is possibly the case with the Industrial super-sector but with so few data points I wouldn't put money on that being the case:

My intention from hereon is to loosely track the portfolio (by setting it up in Stockopedia with a nominal £4000 invested in each share) to gauge how it performs with no tinkering beyond that demanded by corporate actions. It'll certainly be interesting to see how it copes with whatever economic problems crop up and, more importantly, to check if it's able to deliver the rising income that we're looking for. In some respects this doesn't feel like the best time to invest a lump-sum in the market (with it being near its all-time high) but HYPs are not about timing investment decisions; so we'll just have to see how events play out over the next decade or so!

Note: Part 1 of this article can be found here.

Disclosure: the author holds many of the shares covered in this article.